Economic growth of Indonesia in

2012 is at 6.5 % higher than 2011. In 2013, the government projected the economic

growth at 6.4 %. Despite rupiah currency decline to US dollars, Government

still believes that this country has strong fundamental of macroeconomic. GDP

is dominated by local consumption of more than 240 million people. And that

will make several industry such as food, beverage and tobacco is still growing

by demand from inhabitant of this country. Since 2006 until 2010, this sector

has been growing with average growth at 21 %.

i think government must take

action to face decline in rupiah exchange rate to US dollar. For example, rupee

of India which has same problem, the government of India plan to increase their

government spending for infrastructure projects in order to save their

economic.

Indonesia's government actually

has done several actions in facing the currency problem; they did swap

agreement with South Korea and China amounting to US 40 billion to make rupiah

stronger. They also increase government spending for developing and opening

sixty thousands jobs for younger age (50% of total population) in its departments and local governments at entire nations. It will make domestic consumption

stable. With those actions, i think it is still difficult to reach 6.4 % growth

as the target; they have to increase BI rate again, do tight money policy and

investing more money for Infrastructure projects. Those are just my opinion.

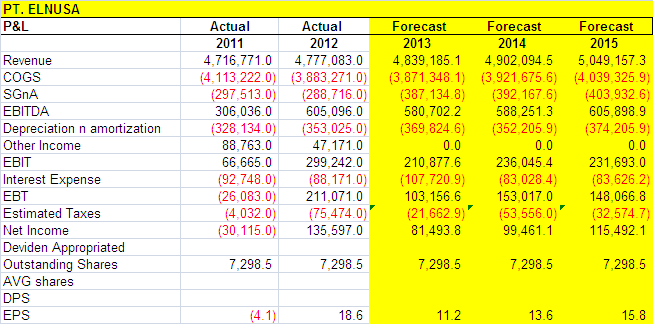

ICBP ( Indofood Consumer Branded Product Sukes Makmur, Tbk )

Indofood CBP (Consumer Branded Product)

sukses makmur Tbk is established as a separate entity in September 2009 and it

did initial public offering in Jakarta Stock Exchange in 2010. The company is a part of group of indofood

which have various business segments in food, beverage and palm oil from

downstream to upstream. This entity operates in packaged food and packaged

beverage for all age.

The products of ICBP have five

segments: noodles, Dairy, Food Seasoning, Snack Food and nutrition and special

food.

The 3 biggest segments in

contribution of revenue of each are 69 % for noodles; 18 % for dairy and 6% for

Snack Food.

For instant noodle, compared to

Thailand, Singapore and Japan, Indonesia has bigger market size and it is still

growing. Since 1999 until to 2009, the instant noodle increase 40 % larger,

from US 2,221 million up in to US 3,191.4 million. i projected the market size

will increase at US 3,600 million in 2013, that means instant noodle is still

having good opportunity to grow.

The instant noodle products of

ICBP are supermi, indomie and sarimie. The strongest competitor for instant

noodle is Wing Food with its Mie Sedap. Based on the data above the number of

player in instant noodle is increase from 2001 at 57 players become 84 players

in 2005.

ICBP need more innovation to

create new product and defend its market share, especially in instant noodle

market size. I think the company has to do more in anticipating price of its

essential commodities, wheat. for example in this recent condition, the commodities

rises in its price because of the weaken currency of rupiah to US, the company

must pay more to buy material for its production. Although the export has been doing for several years but i think it is not significant in number.

in spite of the ICBP is supported

by its affiliate, the biggest wheat flour mills in the world, Bogasari, The

company still need to innovate in others product which use more local

commodities such as rice, cassava, potato or others commodities from the sea. Or

it does acquisition of plantation in Europe to produce wheat. Diversification or vertical integration, two options which is good for the future.

For snack food segment, the sales

contribution tends to increase from 2009 until 2012. it need more concern and

investment in promotion and research to increase revenue.

For Dairy food, its sales

contribution is stable, at 18 - 19 percent. People in indonesia preferred to

consumes instant noodle because of cheaper price to alternate rice which is

more expensive.

I conclude that ICBP need more

investment to enlarge their market size, especially in non noodle product such

as dairy food, beverage or others. There are a lot of cash and cash equivalent in 2010 until 2012.

ICBP has just done its IPO in 2010, the company may still wait for good

momentum to invest. with its liquidity the company could invest new factory or

acquire existing brand from another competitor or doing vertical integration,

such as buying another distributor company or buying packaging / plastic

producer. I don't know its management plan for its future. If the company will late in taking action, the competitor will take chance to expand, I remember when wings food expand its food division with mie sedap. ICPB produce mie sedaaap to face wings food.

The investor need to analyze its

activity ratio, profitability ratio and others

financial ratio to ensure that the company will be more profitable at the next

three years. Transaction with relate parties is needed more concern.

The company have several

creditors, those consist of Bank Mandiri (working capital loan and overdraft

loan), ANZ (Trust Receipt for import ), BCA (MML and working capital loan).

In 2009 - 2012, cash and cash

equivalent increases from 695.8 to 5,484.3 meanwhile net cash flow from

investment activities increases from 307.6 to 1492. The net fixed asset also

increases from 2180.4 to 3,839.8

The net sales in 2012 increase 11

% higher than net sales in 2011. Net income of 2012 is higher than 2011, it

grows 10.4 %.

I make estimate the company will

grow 10 %higher in 2013 based on average growth at the past four year

if there is no merger and acquisition in recent year.

Link and news :

Indofood CBP acquires Club for Rp 2.2 trillion

http://www.thejakartapost.com/news/2013/11/16/indofood-cbp-acquires-club-rp-22-trillion.html

The PCIB Acquisition completed

http://www.indofoodcbp.com/corporate/InvestorRelations/PressReleases/tabid/130/articleType/ArticleView/articleId/84/language/en-US/THE-PCIB-ACQUISITION-COMPLETED.aspx

Board of directors

http://www.indofoodcbp.com/corporate/en-us/ourcompany/management/boardofdirectors.aspx